|

|

2 weeks ago | |

|---|---|---|

| .. | ||

| solution | 3 weeks ago | |

| working | 3 weeks ago | |

| README.md | 2 weeks ago | |

| assignment.md | 3 weeks ago | |

README.md

使用支持向量回归器进行时间序列预测

在上一节课中,你学习了如何使用 ARIMA 模型进行时间序列预测。现在,你将学习支持向量回归器(Support Vector Regressor, SVR)模型,这是一种用于预测连续数据的回归模型。

课前测验

介绍

在本课中,你将学习如何使用SVM(支持向量机)构建回归模型,即SVR(支持向量回归器)。

时间序列中的 SVR 1

在理解 SVR 在时间序列预测中的重要性之前,你需要了解以下几个关键概念:

- 回归(Regression): 一种监督学习技术,用于根据给定的输入集预测连续值。其核心思想是拟合一条曲线(或直线),使其尽可能多地通过数据点。点击这里了解更多信息。

- 支持向量机(SVM): 一种监督学习模型,可用于分类、回归和异常值检测。SVM 模型在特征空间中是一条超平面,在分类任务中充当边界,在回归任务中充当最佳拟合线。SVM 通常使用核函数将数据集转换到更高维的空间,以便更容易分离。点击这里了解更多关于 SVM 的信息。

- 支持向量回归器(SVR): SVM 的一种变体,用于找到最佳拟合线(在 SVM 中是超平面),使其尽可能多地通过数据点。

为什么选择 SVR?1

在上一节课中,你学习了 ARIMA,这是一种非常成功的统计线性方法,用于预测时间序列数据。然而,在许多情况下,时间序列数据具有非线性特性,这种特性无法通过线性模型映射。在这种情况下,SVM 在回归任务中处理数据非线性的能力使得 SVR 在时间序列预测中非常成功。

练习 - 构建一个 SVR 模型

数据准备的前几步与上一节关于 ARIMA 的内容相同。

打开本课的 /working 文件夹,找到 notebook.ipynb 文件。2

-

运行 notebook 并导入必要的库:2

import sys sys.path.append('../../')import os import warnings import matplotlib.pyplot as plt import numpy as np import pandas as pd import datetime as dt import math from sklearn.svm import SVR from sklearn.preprocessing import MinMaxScaler from common.utils import load_data, mape -

从

/data/energy.csv文件中加载数据到 Pandas 数据框中并查看:2energy = load_data('../../data')[['load']] -

绘制 2012 年 1 月至 2014 年 12 月的所有能源数据:2

energy.plot(y='load', subplots=True, figsize=(15, 8), fontsize=12) plt.xlabel('timestamp', fontsize=12) plt.ylabel('load', fontsize=12) plt.show()

现在,让我们构建 SVR 模型。

创建训练集和测试集

现在数据已经加载,你可以将其分为训练集和测试集。接着,你需要对数据进行重塑,以创建基于时间步长的数据集,这是 SVR 所需的。你将在训练集上训练模型。训练完成后,你将在训练集、测试集以及完整数据集上评估模型的准确性,以查看整体性能。需要确保测试集覆盖的时间段晚于训练集,以避免模型从未来时间段中获取信息2(这种情况称为过拟合)。

-

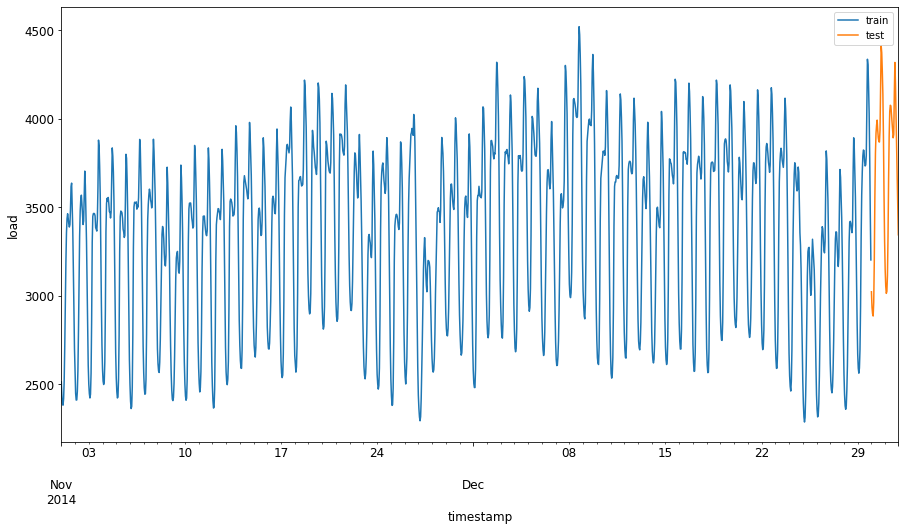

将 2014 年 9 月 1 日至 10 月 31 日的两个月数据分配给训练集。测试集将包括 2014 年 11 月 1 日至 12 月 31 日的两个月数据:2

train_start_dt = '2014-11-01 00:00:00' test_start_dt = '2014-12-30 00:00:00' -

可视化差异:2

energy[(energy.index < test_start_dt) & (energy.index >= train_start_dt)][['load']].rename(columns={'load':'train'}) \ .join(energy[test_start_dt:][['load']].rename(columns={'load':'test'}), how='outer') \ .plot(y=['train', 'test'], figsize=(15, 8), fontsize=12) plt.xlabel('timestamp', fontsize=12) plt.ylabel('load', fontsize=12) plt.show()

准备训练数据

现在,你需要通过过滤和缩放数据来准备训练数据。过滤数据集以仅包含所需的时间段和列,并通过缩放将数据投影到 0 到 1 的区间内。

-

过滤原始数据集,仅包含上述时间段的数据集,并仅保留所需的“load”列和日期:2

train = energy.copy()[(energy.index >= train_start_dt) & (energy.index < test_start_dt)][['load']] test = energy.copy()[energy.index >= test_start_dt][['load']] print('Training data shape: ', train.shape) print('Test data shape: ', test.shape)Training data shape: (1416, 1) Test data shape: (48, 1) -

将训练数据缩放到 (0, 1) 区间:2

scaler = MinMaxScaler() train['load'] = scaler.fit_transform(train) -

现在,缩放测试数据:2

test['load'] = scaler.transform(test)

创建基于时间步长的数据 1

对于 SVR,你需要将输入数据转换为 [batch, timesteps] 的形式。因此,你需要重塑现有的 train_data 和 test_data,以便创建一个新的维度来表示时间步长。

# Converting to numpy arrays

train_data = train.values

test_data = test.values

在本例中,我们设置 timesteps = 5。因此,模型的输入是前 4 个时间步的数据,输出是第 5 个时间步的数据。

timesteps=5

使用嵌套列表推导将训练数据转换为二维张量:

train_data_timesteps=np.array([[j for j in train_data[i:i+timesteps]] for i in range(0,len(train_data)-timesteps+1)])[:,:,0]

train_data_timesteps.shape

(1412, 5)

将测试数据转换为二维张量:

test_data_timesteps=np.array([[j for j in test_data[i:i+timesteps]] for i in range(0,len(test_data)-timesteps+1)])[:,:,0]

test_data_timesteps.shape

(44, 5)

从训练数据和测试数据中选择输入和输出:

x_train, y_train = train_data_timesteps[:,:timesteps-1],train_data_timesteps[:,[timesteps-1]]

x_test, y_test = test_data_timesteps[:,:timesteps-1],test_data_timesteps[:,[timesteps-1]]

print(x_train.shape, y_train.shape)

print(x_test.shape, y_test.shape)

(1412, 4) (1412, 1)

(44, 4) (44, 1)

实现 SVR 1

现在是时候实现 SVR 了。要了解更多关于此实现的信息,你可以参考此文档。在我们的实现中,我们遵循以下步骤:

- 调用

SVR()并传入模型超参数:kernel、gamma、C 和 epsilon 来定义模型。 - 调用

fit()函数准备训练数据。 - 调用

predict()函数进行预测。

现在我们创建一个 SVR 模型。在这里,我们使用 RBF 核函数,并将超参数 gamma、C 和 epsilon 分别设置为 0.5、10 和 0.05。

model = SVR(kernel='rbf',gamma=0.5, C=10, epsilon = 0.05)

在训练数据上拟合模型 1

model.fit(x_train, y_train[:,0])

SVR(C=10, cache_size=200, coef0=0.0, degree=3, epsilon=0.05, gamma=0.5,

kernel='rbf', max_iter=-1, shrinking=True, tol=0.001, verbose=False)

进行模型预测 1

y_train_pred = model.predict(x_train).reshape(-1,1)

y_test_pred = model.predict(x_test).reshape(-1,1)

print(y_train_pred.shape, y_test_pred.shape)

(1412, 1) (44, 1)

你已经构建了 SVR!现在我们需要对其进行评估。

评估模型 1

为了评估模型,首先我们需要将数据缩放回原始比例。然后,为了检查性能,我们将绘制原始数据和预测数据的时间序列图,并打印 MAPE 结果。

将预测值和原始输出缩放回原始比例:

# Scaling the predictions

y_train_pred = scaler.inverse_transform(y_train_pred)

y_test_pred = scaler.inverse_transform(y_test_pred)

print(len(y_train_pred), len(y_test_pred))

# Scaling the original values

y_train = scaler.inverse_transform(y_train)

y_test = scaler.inverse_transform(y_test)

print(len(y_train), len(y_test))

检查模型在训练数据和测试数据上的性能 1

我们从数据集中提取时间戳,以显示在图表的 x 轴上。注意,我们使用前 timesteps-1 个值作为第一个输出的输入,因此输出的时间戳将从那之后开始。

train_timestamps = energy[(energy.index < test_start_dt) & (energy.index >= train_start_dt)].index[timesteps-1:]

test_timestamps = energy[test_start_dt:].index[timesteps-1:]

print(len(train_timestamps), len(test_timestamps))

1412 44

绘制训练数据的预测结果:

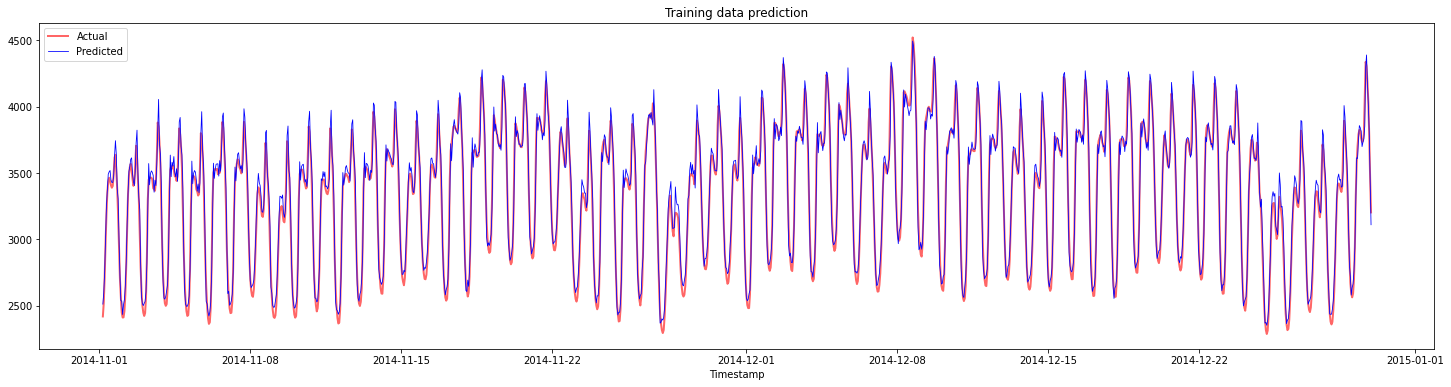

plt.figure(figsize=(25,6))

plt.plot(train_timestamps, y_train, color = 'red', linewidth=2.0, alpha = 0.6)

plt.plot(train_timestamps, y_train_pred, color = 'blue', linewidth=0.8)

plt.legend(['Actual','Predicted'])

plt.xlabel('Timestamp')

plt.title("Training data prediction")

plt.show()

打印训练数据的 MAPE:

print('MAPE for training data: ', mape(y_train_pred, y_train)*100, '%')

MAPE for training data: 1.7195710200875551 %

绘制测试数据的预测结果:

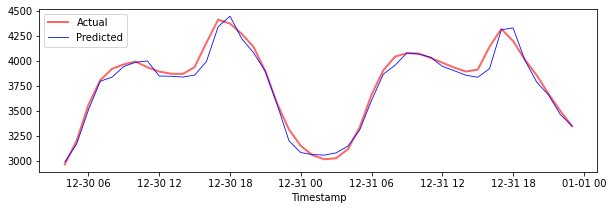

plt.figure(figsize=(10,3))

plt.plot(test_timestamps, y_test, color = 'red', linewidth=2.0, alpha = 0.6)

plt.plot(test_timestamps, y_test_pred, color = 'blue', linewidth=0.8)

plt.legend(['Actual','Predicted'])

plt.xlabel('Timestamp')

plt.show()

打印测试数据的 MAPE:

print('MAPE for testing data: ', mape(y_test_pred, y_test)*100, '%')

MAPE for testing data: 1.2623790187854018 %

🏆 你在测试数据集上取得了非常好的结果!

检查模型在完整数据集上的性能 1

# Extracting load values as numpy array

data = energy.copy().values

# Scaling

data = scaler.transform(data)

# Transforming to 2D tensor as per model input requirement

data_timesteps=np.array([[j for j in data[i:i+timesteps]] for i in range(0,len(data)-timesteps+1)])[:,:,0]

print("Tensor shape: ", data_timesteps.shape)

# Selecting inputs and outputs from data

X, Y = data_timesteps[:,:timesteps-1],data_timesteps[:,[timesteps-1]]

print("X shape: ", X.shape,"\nY shape: ", Y.shape)

Tensor shape: (26300, 5)

X shape: (26300, 4)

Y shape: (26300, 1)

# Make model predictions

Y_pred = model.predict(X).reshape(-1,1)

# Inverse scale and reshape

Y_pred = scaler.inverse_transform(Y_pred)

Y = scaler.inverse_transform(Y)

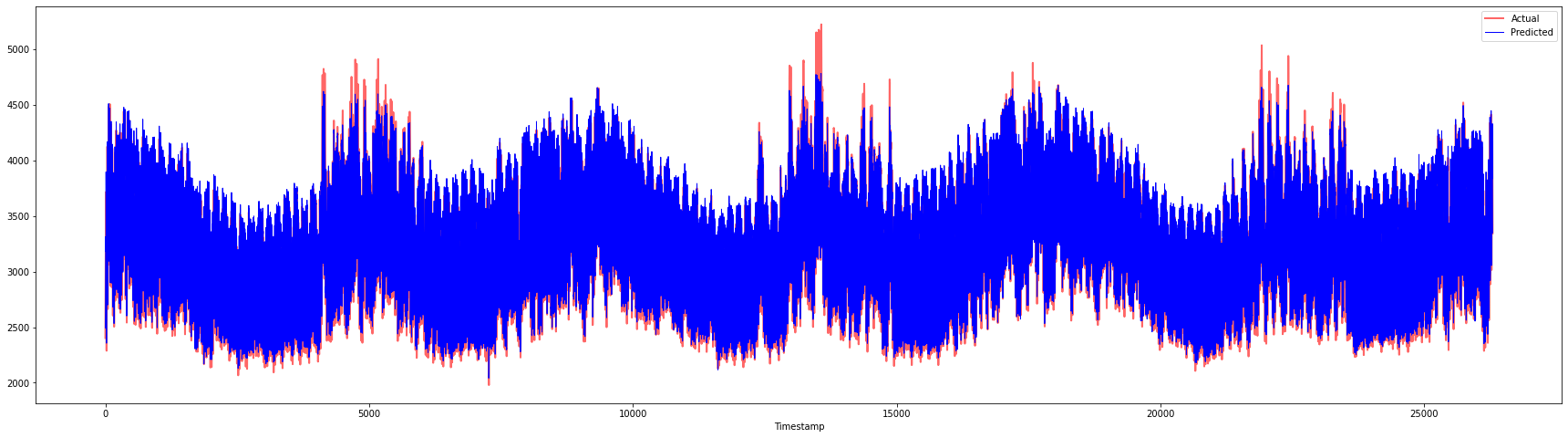

plt.figure(figsize=(30,8))

plt.plot(Y, color = 'red', linewidth=2.0, alpha = 0.6)

plt.plot(Y_pred, color = 'blue', linewidth=0.8)

plt.legend(['Actual','Predicted'])

plt.xlabel('Timestamp')

plt.show()

print('MAPE: ', mape(Y_pred, Y)*100, '%')

MAPE: 2.0572089029888656 %

🏆 非常棒的图表,显示了一个具有良好准确性的模型。干得好!

🚀挑战

- 尝试在创建模型时调整超参数(gamma、C、epsilon),并在数据上进行评估,看看哪组超参数在测试数据上表现最佳。要了解更多关于这些超参数的信息,你可以参考这里的文档。

- 尝试为模型使用不同的核函数,并分析它们在数据集上的表现。相关文档可以参考这里。

- 尝试为模型设置不同的

timesteps值,观察模型在预测时的表现。

课后测验

复习与自学

本课旨在介绍 SVR 在时间序列预测中的应用。要了解更多关于 SVR 的信息,你可以参考这篇博客。scikit-learn 的文档提供了关于 SVM 的更全面解释,包括 SVR 和其他实现细节,例如可以使用的不同核函数及其参数。

作业

致谢

免责声明:

本文档使用AI翻译服务 Co-op Translator 进行翻译。尽管我们努力确保翻译的准确性,但请注意,自动翻译可能包含错误或不准确之处。原始语言的文档应被视为权威来源。对于关键信息,建议使用专业人工翻译。我们不对因使用此翻译而产生的任何误解或误读承担责任。

-

本节中的文本、代码和输出由 @AnirbanMukherjeeXD 提供 ↩︎